Land Tax in India: What NRIs & HNIs Must Know

15 May 2026

Land tax in India involves multiple charges, including property tax, stamp duty, and capital gains tax. These taxes are levied at various stages by the state and central governments and municipal bodies. A TDS is also applicable when an NRI sells a property.

For many Non-Resident Indians (NRIs), owning land in India represents security, legacy, and long-term growth. Beyond the purchase price lies a complex layer of costs, including property tax, recurring land tax payments, and compliance requirements that need to be properly understood.

This is where understanding “what is property tax in India” becomes critical. A clear grasp of these aspects can help you plan better, avoid penalties, and make smarter real estate decisions.

In this blog, we will break down the key rules, costs, and compliance requirements that every NRI and HNI should know before buying land in India.

Can NRIs Buy Land in India?

As per Sections 5 and 6 of the Foreign Exchange Management Act (FEMA) of 1999, NRIs are allowed to buy residential and commercial properties in India. These include land, buildings, apartments, and other types of real estate. However, buying agricultural land, farmhouses, and plantations is not permitted.

Additionally, you must follow all legal guidelines, obtain the Reserve Bank of India’s (RBI) approval, and complete proper documentation to ensure your purchase is fully compliant and hassle-free.

Understanding Land Tax in India

Land tax in India is not a single, uniform levy. It refers to multiple taxes and charges levied by the state and central governments and local authorities at various points. The amount may vary by location, land classification, and usage.

A plot in an urban area is taxed differently from one in a rural zone. Similarly, developed land may be subject to different taxes than vacant land. It is highly crucial to understand this framework before making a purchase decision.

Is There Any Tax on Buying Property?

As an NRI planning to purchase land in India, the registration fee is most probably the first tax you are going to pay. It is calculated based on the assessed value of the property and is levied by the municipal corporation or local governing bodies. The rate may vary by state and city. It may also depend on the property's location, size, age, and condition.

Apart from the property tax, a stamp duty is also levied. It typically ranges from 3% to 8%, depending on the state and property type.

**Are There Any Recurring Property Tax Payments? ** Besides a one-time tax on buying property, you may also have to pay certain recurring taxes. The most common is property tax, which is paid annually to the local authority or municipal body. The amount depends on how the property is valued under local rules. Each municipality has its own method to determine property taxes.

In some cases, additional land tax payments may apply based on the type of land.

Is Capital Gains Tax Also Applicable?

The capital gains tax is not levied at the time of purchase, but at the time of sale of the property. The rate depends on how long you have held the property before selling it. Here’s how to calculate property gain tax:

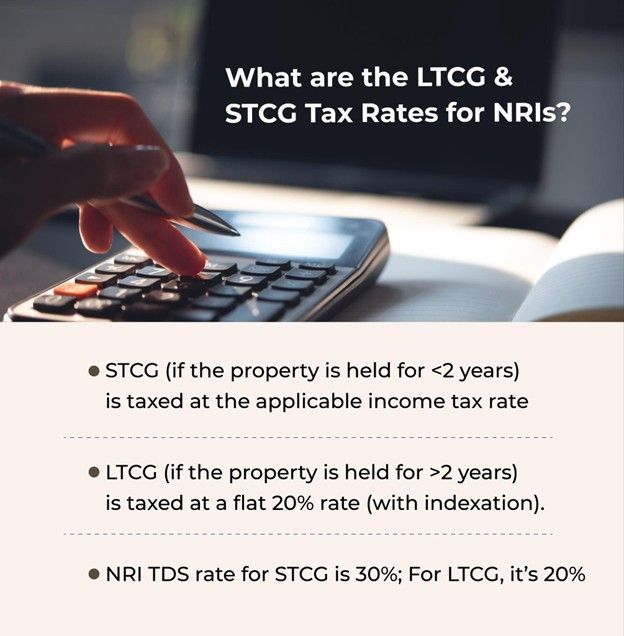

If you have held the property for two years or less before selling, gains are classified as Short-Term Capital Gains (STCG). They are added to your taxable income and taxed as per the applicable slab rate.

If you have held the property for more than two years before selling, gains are classified as Long-Term Capital Gains (LTCG). They are taxed at a 20% rate (with indexation).

However, under Sections 54 and 54F of the Income Tax Act, NRIs are eligible for capital gains tax exemptions. To avail of this exemption, you must reinvest the gains in a residential property.

NRI Specific Rules: TDS And Compliance

Under Section 195 of the Income Tax Act, a buyer is required to deduct TDS (Tax Deducted at Source) while making a payment to an NRI. This rule is mandatory, irrespective of the property’s type or value. The NRI TDS rate is higher than the resident rate.

For short-term gains, i.e., where the holding period is less than two years, the rate for TDS on NRI property is 30%. For long-term gains, this rate is 20%.

The Bottom Line

Land remains a strong long-term asset in India. However, returns depend on more than price appreciation. Land tax in India, including property tax, TDS, and capital gains, plays a key role in the final outcome.

For NRIs and HNIs, understanding the full tax architecture around Indian land ownership is the difference between a clean, profitable exit and a complicated, cost-heavy one.

The House of Abhinandan Lodha follows a transparent approach to this process. In destinations such as Anjarle, Goa, Ayodhya, and Vrindavan, investors are given clarity on costs and tax obligations upfront. This ensures that decisions are made with full information rather than assumptions.

FAQs

1. How to pay property tax online?

You can pay property tax online through the local municipal corporation’s website. The payment can be made through a debit card, credit card, NetBanking, or UPI.

2. Are tax rates the same for residential and commercial properties?

No, the tax rates for commercial properties are usually higher than those for residential properties. It’s because commercial properties are used to generate revenue.

3. How often do I need to pay property tax?

Property tax is usually paid annually. The payment frequency may vary based on the local municipality’s guidelines.

4. Can I claim tax exemptions on land tax payments?

Yes, you can claim tax exemption on capital gains under Sections 54 and 54F. However, no tax exemptions are available on property tax payments.

5. Can NRIs take a loan for purchasing land in India?

Yes, NRIs can apply for loans to buy land in India.

Related Blogs

Best Long-Term Investment Plans for HNI Investment in India

09 Apr 2026

FD vs Mutual Fund vs Coastal Land Investment: Which Investment is Best?

06 Apr 2026

How to Invest in Real Estate: Best Places to Buy Land for Sale in India

13 May 2026